Life Insurance Myths: Debunked

Three important factors when it comes to your financial life.

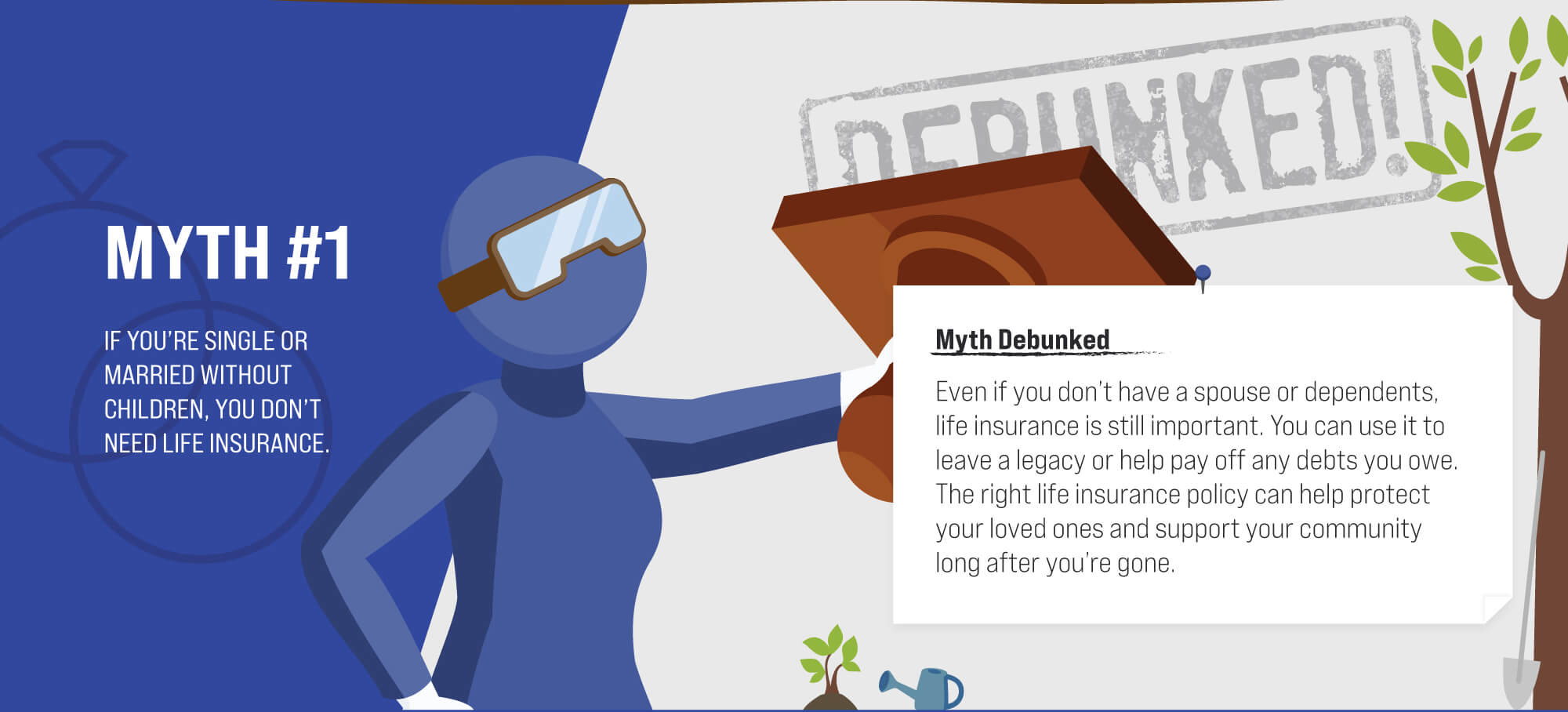

Start taking proactive measures to safeguard your legacy and plan for your family’s financial future.

Are you rethinking how you'll give back in retirement? Consider these opportunities that don’t require financial commitment.